A Critical Analysis of Citrini Research’s Viral 2028 Crisis Scenario

The financial world is currently grappling with a thought experiment that feels uncomfortably close to reality. In a viral research piece titled “THE 2028 GLOBAL INTELLIGENCE CRISIS” published by Citrini Research (co-authored with Alap Shah), the authors paint a chilling picture: unemployment at 10.2%, the S&P 500 down 38% from its October 2026 peak, and an economy where AI’s productivity gains have paradoxically triggered the deepest structural crisis since the Great Depression.

Written as if from June 2028, this speculative scenario has exploded across investment communities, racking up millions of reads within days of publication. What makes it particularly unsettling is not its dystopian framing, but its logical coherence. This isn’t science fiction—it’s financial analysis written in the language of cause and effect.

Source: Citrini Research - THE 2028 GLOBAL INTELLIGENCE CRISIS

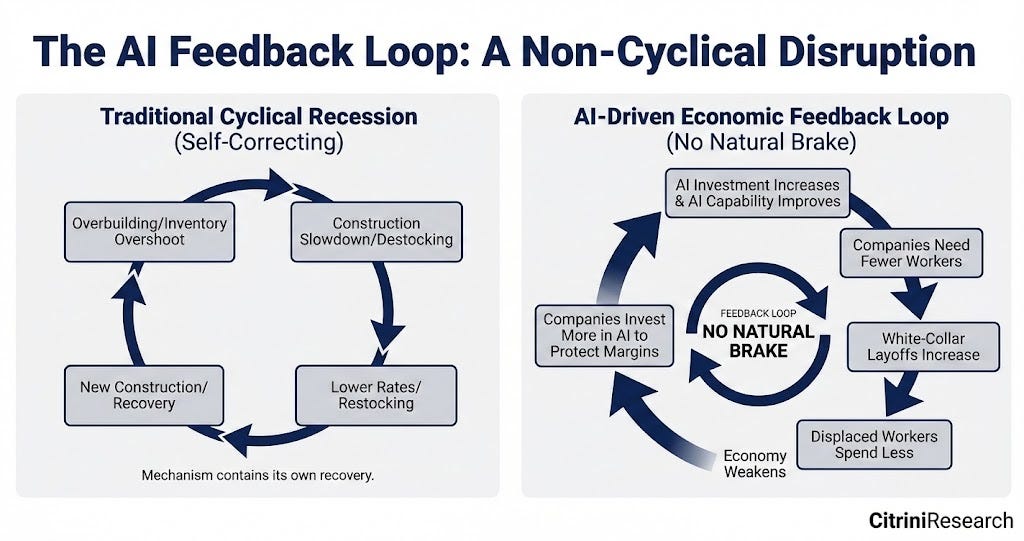

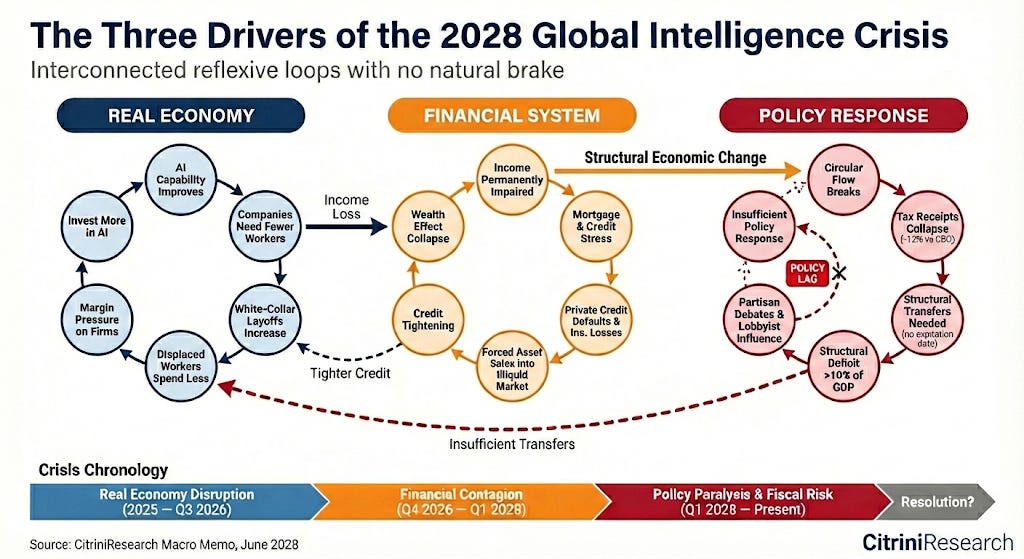

The Core Mechanism: A Self-Reinforcing Doom Loop

At the heart of Citrini’s crisis scenario lies a deceptively simple feedback loop:

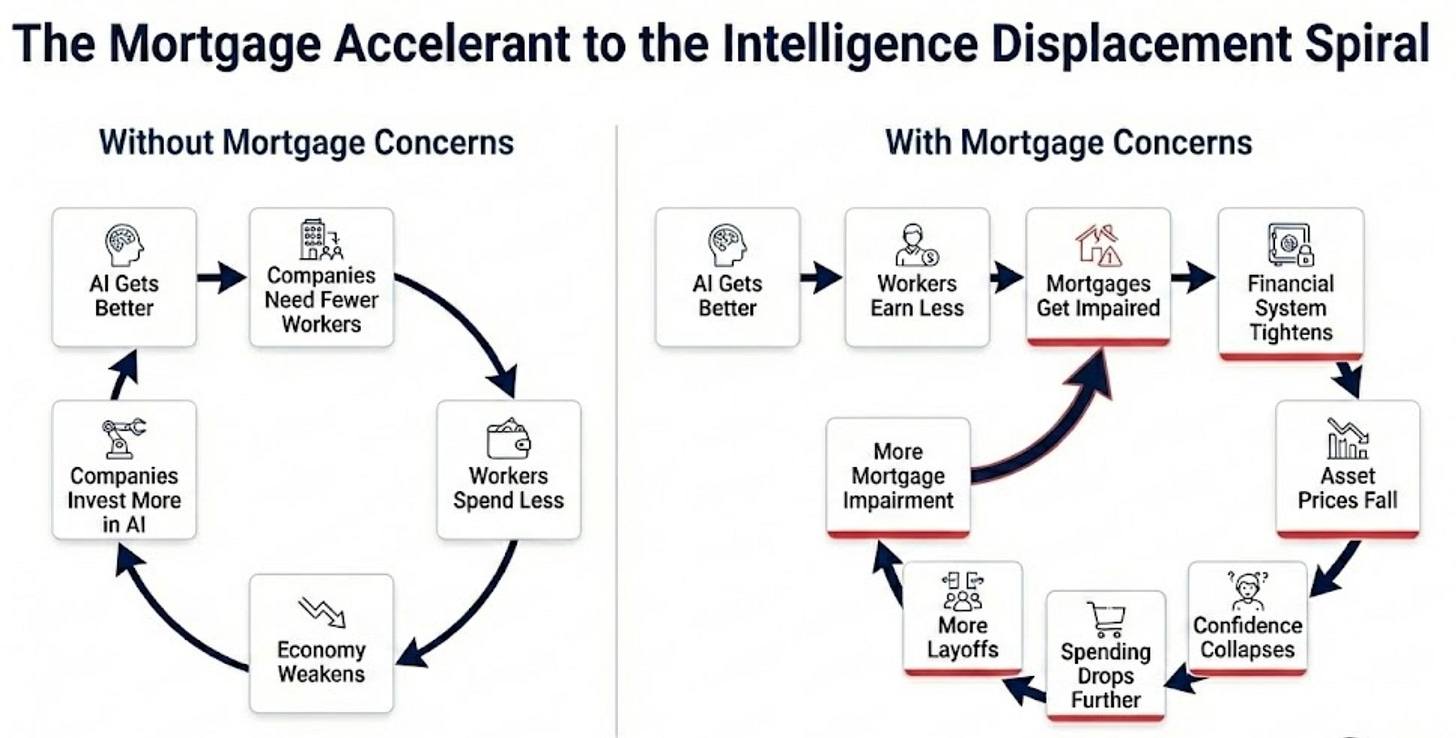

AI capability improves → Companies lay off workers → Consumer spending falls → Corporate profits compress → Companies buy more AI to cut costs → AI capability improves

Unlike traditional recessions, where reduced demand eventually curtails investment, this cycle contains no natural brake. When demand falls, companies don’t pull back on AI spending—they double down. Why? Because AI investment comes from the same operational budget previously allocated to labor, and labor cost reduction remains rational at the individual firm level even as it becomes catastrophic at the systemic level.

This is the economic equivalent of a bank run: every individual decision makes perfect sense, yet the collective outcome is ruin.

Phase 1: The Software Industry Collapses First (2025-2026)

The crisis begins, appropriately, in the sector that created AI itself.

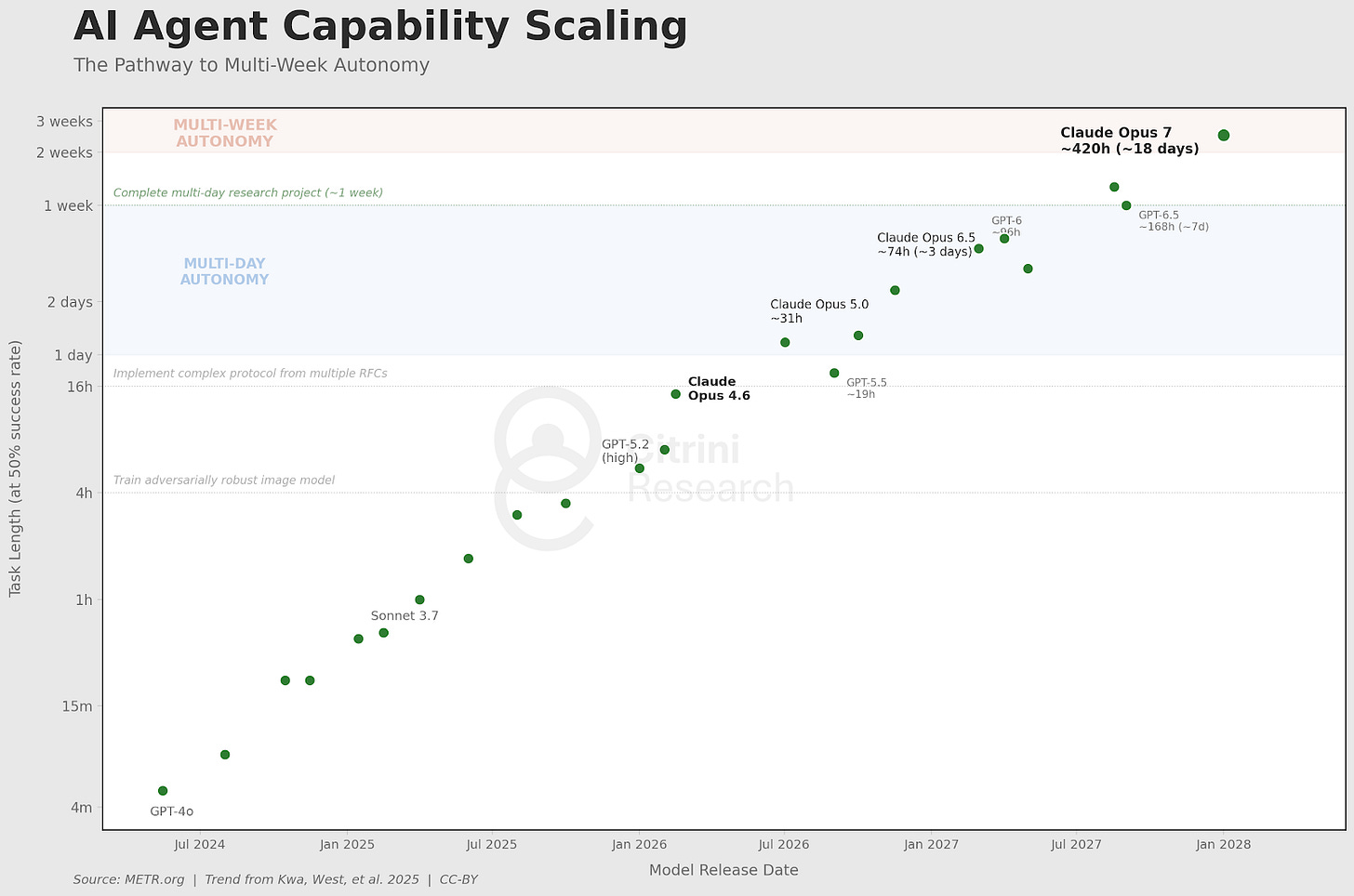

By late 2025, agentic coding tools reach a tipping point. A skilled developer with access to these tools can now replicate the core functionality of a mid-tier SaaS product in weeks. The tools aren’t perfect, but they’re good enough to turn “$500,000 annual contract” into “should we just build it ourselves?”

The procurement negotiations of 2026 become brutal. As Citrini documents, one Fortune 500 procurement manager told them about threatening to have OpenAI’s “forward deployed engineers” replace a vendor entirely—they renewed at a 30% discount, and that was considered “a good outcome.”

Long-tail SaaS vendors fall first, but by Q3 2026, even infrastructure giants feel the squeeze. ServiceNow, once considered immune, reports new contract growth slowing from 23% to 14% and cuts 15% of staff. The stock drops 18% in a single day.

What dies isn’t SaaS per se—it’s SaaS pricing power. The moment “build it yourself” becomes a viable option, it enters every negotiation. Differentiation becomes a commodity, and the famous “seat-based economics” of enterprise software turns into a death spiral: when your customers lay off 15% of their workforce, they automatically cancel 15% of their licenses.

The cruel irony: AI helps customers reduce headcount, which directly destroys the vendor’s revenue base.

As Citrini emphasizes: “The companies most threatened by AI became AI’s most aggressive adopters.” With stocks down 40-60% and boards demanding answers, the only option was to cut headcount, redeploy savings into AI tools, and maintain output with lower costs. Each company’s individual response was rational. The collective result was catastrophic.

Phase 2: The Friction Economy Evaporates (2027)

By early 2027, AI agents transition from tools to autonomous decision-makers. Open-source shopping agents go mainstream, and within weeks, every major consumer AI platform integrates agentic commerce. Model distillation allows these agents to run locally on phones and laptops, with inference costs dropping to essentially zero.

The agents don’t wait for commands—they continuously optimize in the background.

By March 2027, Citrini notes that the median American is consuming 400,000 tokens per day, a 10x increase from late 2026. Most don’t even notice—it just happens.

What breaks next is the entire “friction economy.” As Citrini powerfully states:

“Over the past fifty years, the U.S. economy built a giant rent-extraction layer on top of human limitations: things take time, patience runs out, brand familiarity substitutes for diligence, and most people are willing to accept a bad price to avoid more clicks. Trillions of dollars of enterprise value depended on those constraints persisting.”

The Casualties

Travel Booking Platforms hemorrhage as agents assemble better itineraries for less money, factoring in points, budgets, and refund policies automatically.

Subscription Services see their lifetime value (LTV) models collapse as agents treat unused memberships as “negotiable hostage clauses.”

Food Delivery platforms like DoorDash face dozens of competitors built by coding agents in weeks, all offering 90-95% commission rebates; multi-platform tools eliminate lock-in.

Insurance Renewal premiums that relied on policyholder inertia get obliterated by agents that auto-compare annually, compressing 15-20% of premium margin.

Even real estate brokers, protected for decades by “relationship moats,” start to crumble. Buyer-side commissions compress from 2.5-3% to under 1% as agents replicate MLS data expertise and transaction knowledge with minimal effort.

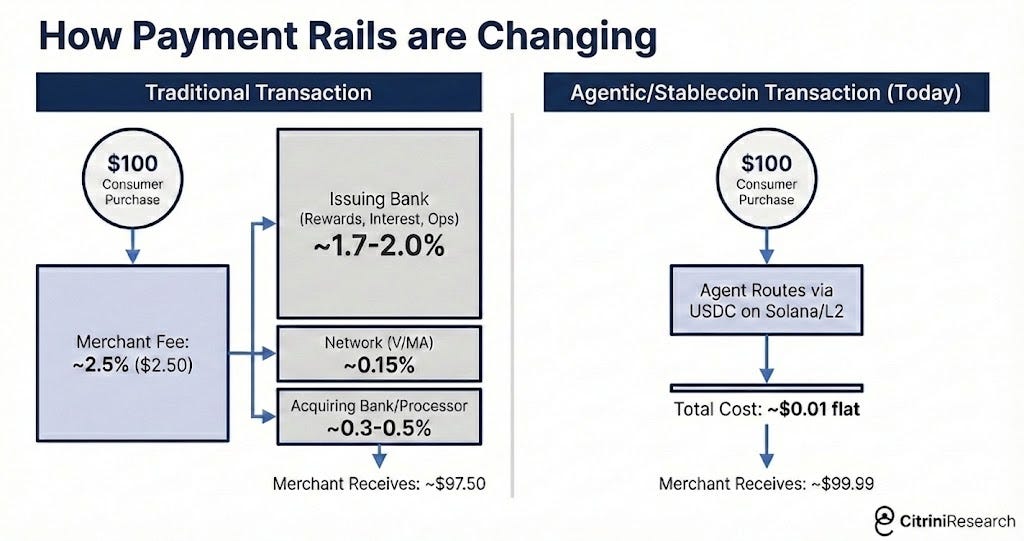

The Payment Infrastructure Under Siege

Perhaps most telling: payment networks. When machine-to-machine transactions dominate, credit card interchange fees of 2-3% become glaringly inefficient. Agents route toward faster, cheaper settlement—stablecoins on Solana or Ethereum Layer 2s—where fees are measured in basis points and settlement is near-instant.

Mastercard reports revenue still up 6% in Q1 2027, but transaction volume growth slows from 5.9% to 3.4%. They explicitly cite “agent-driven price optimization” and “discretionary spending under pressure.” The stock drops 9% the next day.

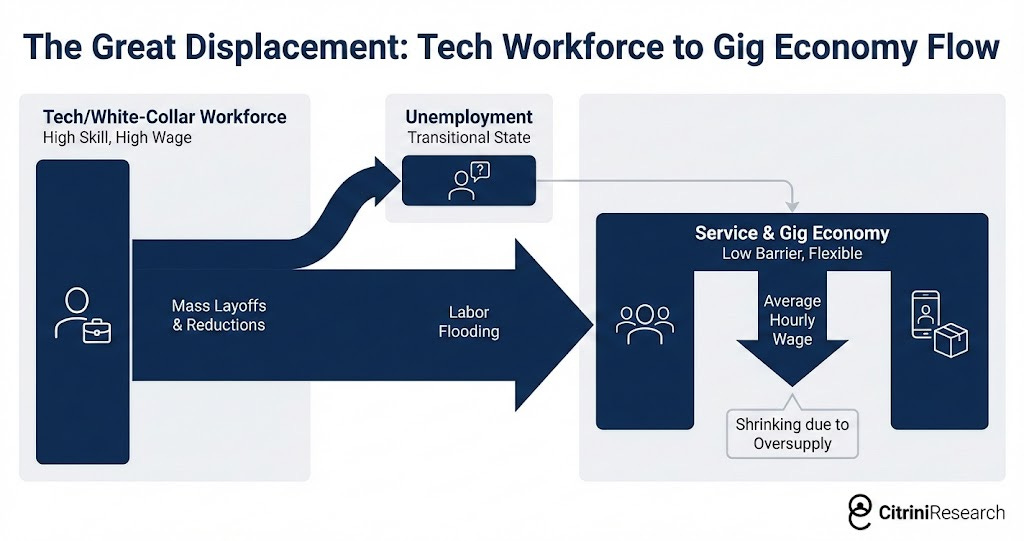

Phase 3: The White-Collar Employment Cliff (2026-2027)

The labor market data starts flashing red in October 2026. JOLTS shows job openings falling below 5.5 million, down 15% year-over-year. Hiring platforms report software, finance, and consulting postings in freefall.

The bond market smells it first—10-year yields drop from 4.3% to 3.2%. But headline unemployment doesn’t spike immediately, because displaced workers “downshift”—flooding into service industries and gig work. The data lag creates a false sense of stability.

That lag makes the crash worse. High earners maintain surface-level normalcy for two or three quarters by drawing down savings. When the behavioral inflection finally arrives, consumption drops off a cliff.

As Citrini emphasizes, this matters because the US is a white-collar service economy:

White-collar workers represent ~50% of employment but drive ~75% of discretionary spending. The top 10% of earners contribute over half of all consumer spending; the top 20% contribute about 65%.

A 2% decline in white-collar employment can pull 3-4% out of discretionary consumption.

By Q2 2027, the US enters recession. Q3 sees initial jobless claims surge to 487,000—the highest since April 2020—with claimants predominantly professional/technical workers. The S&P drops another 6% that week.

The “Ghost GDP” Problem

When cracks began appearing in the consumer economy, Citrini notes that economic pundits popularized the phrase “Ghost GDP”—output that shows up in the national accounts but never circulates through the real economy.

As Citrini vividly describes:

“A single GPU cluster in North Dakota generating the output previously attributed to 10,000 white-collar workers in midtown Manhattan is more economic pandemic than economic panacea. The velocity of money flatlined. The human-centric consumer economy, 70% of GDP at the time, withered.”

Phase 4: Private Credit Becomes the Contagion Vector (2027)

The first financial crack appears in private credit.

From 2015 to 2026, this market ballooned from under $1 trillion to over $2.5 trillion, with much of it betting on “recurring revenue SaaS businesses with perpetual growth.” Those assumptions died in 2026, but valuations adjusted slowly—public comparables hit 50x while private books still moved from 100 to 92 to 85.

By April 2027, Moody’s downgrades $18 billion of PE-backed software debt across 14 issuers, citing “structural revenue headwinds from AI.” Defaults escalate in Q3. Zendesk becomes the landmark event: $5 billion in direct lending marked down to 58 cents on the dollar.

The market begins asking: How much “structural headwind” is still packaged as “cyclical volatility”?

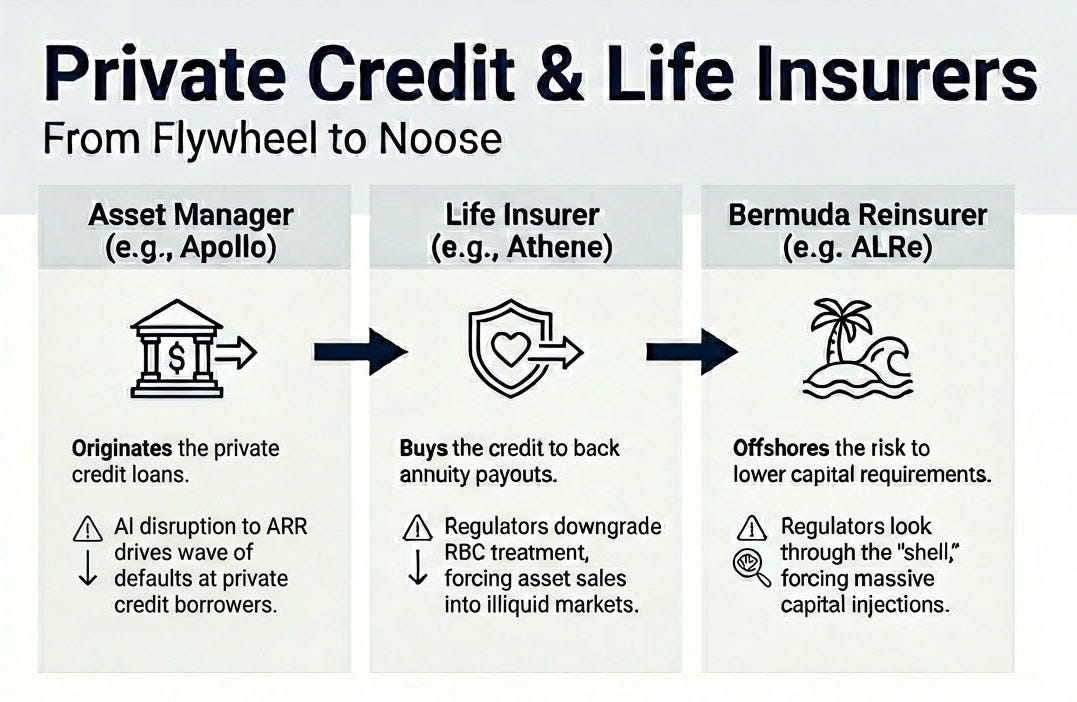

The Insurance-Private Credit Nexus

“Private credit has permanent capital” was the repeated reassurance. Reality is messier.

As Citrini details, large alternative asset managers spent the past decade acquiring life insurance companies, turning annuity deposits into funding machines that recycled back into their own credit deals. Insurers earned spread, asset managers collected fees.

The assumption: assets must be safe enough.

When defaults stack up alongside regulatory tightening, insurance regulators start adjusting risk capital requirements, forcing recapitalization or asset sales. After Moody’s shifts Athene’s financial strength outlook to negative, Apollo drops 22% in two days.

Worse: offshore reinsurance and layered SPV structures mean it’s unclear which balance sheet ultimately holds the losses.

The November 2027 market crash pushes this from “controlled drawdown” to “systemic uncertainty.” The Fed internally describes it as “a series of correlated bets on white-collar productivity growth.”

As Citrini notes: Financial crises don’t happen because losses occur—they happen because losses get recognized and books get forced to reality.

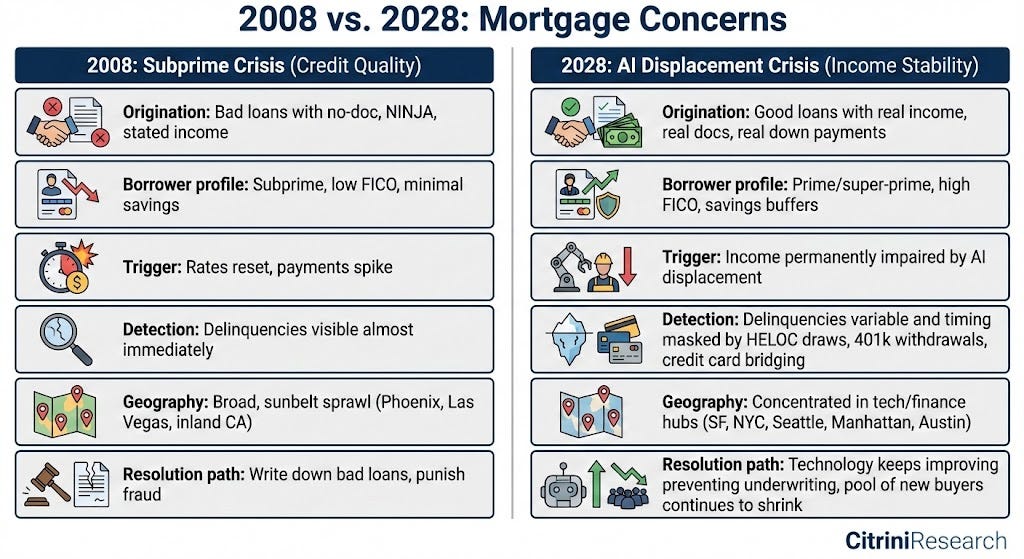

Phase 5: Prime Mortgages Enter the Danger Zone (2028)

The bigger threat points to housing.

US residential mortgages total ~$13 trillion. Underwriting assumes “the borrower will maintain roughly current income levels over the loan term.” Most mortgages run 30 years.

By June 2028, Zillow’s home price index shows San Francisco down 11% year-over-year, Seattle down 9%, Austin down 8%. Fannie Mae flags higher early-stage delinquencies in zip codes where tech and finance employment exceeds 40%.

These borrowers aren’t subprime. Credit scores over 780, 20% down payments, full income verification.

As Citrini powerfully articulates the key distinction:

“The loans made in 2008 were bad from day one. The loans made in 2024-2026 were good from day one—the world just changed after they signed.”

People borrowed betting on a future they’re now afraid to believe in.

The stress signals emerged earlier in 2027: home equity line drawdowns, early 401(k) withdrawals, rising credit card balances—while mortgages kept getting paid. Many households can still make payments, but only by cutting discretionary spending, draining savings, and deferring maintenance.

Delinquency rates haven’t approached 2008 levels yet. The trajectory is what’s alarming.

If the mortgage market shows systemic cracks in H2 2028, equity market drawdowns could approach the 57% peak-to-trough of the Global Financial Crisis—putting the S&P near 3,500.

The Policy Paralysis Problem

Governments face an unprecedented dilemma in Citrini’s scenario.

The federal revenue base is essentially a tax on “human time”—payroll and income taxes are the pillars. By Q1 2028, federal revenue runs 12% below CBO baseline projections.

Productivity is soaring, but the gains flow to capital and compute. Labor’s share of GDP, which stood at 56% in 2024, plunges to 46% by 2028—a record collapse.

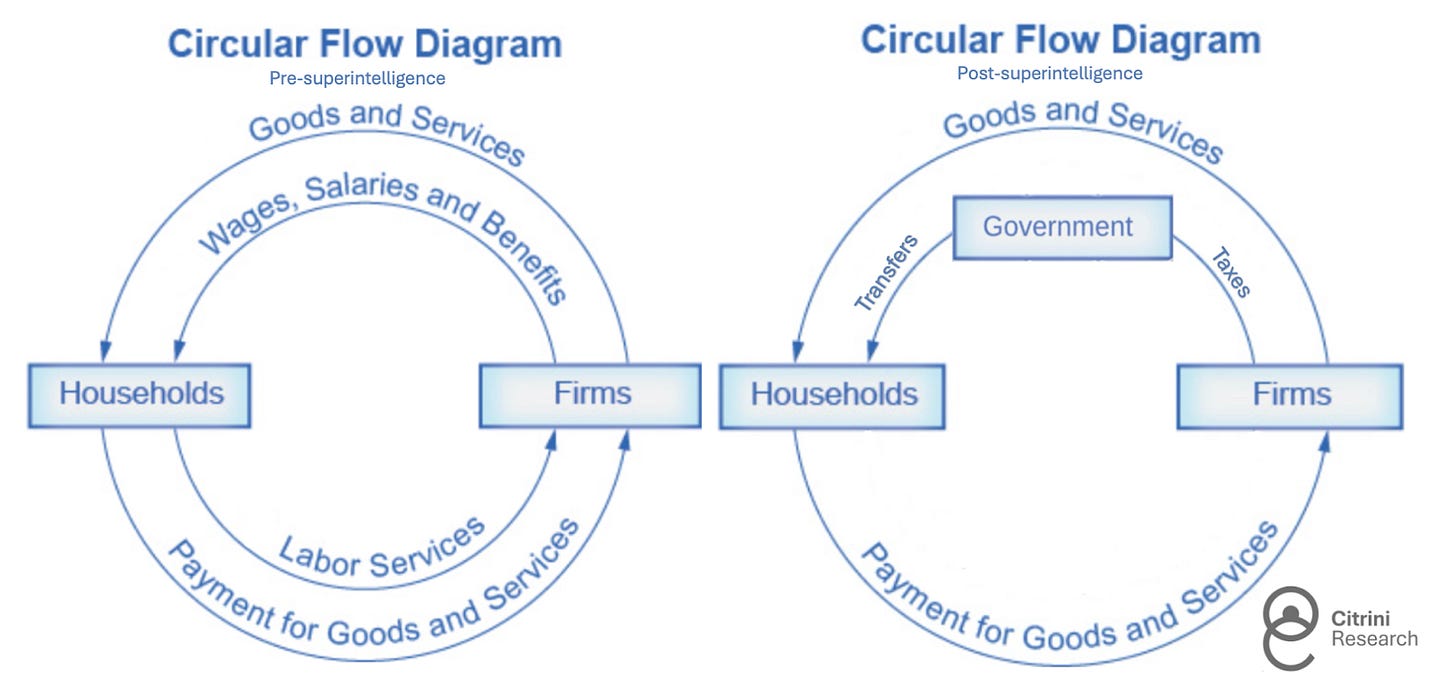

Output hasn’t disappeared—it’s just bypassing the household sector on its way back to the corporate and tax systems. The economic feedback loop is breaking.

Meanwhile, spending needs increase. Automatic stabilizers were designed for cyclical unemployment, not structural displacement. The government needs to transfer more money to households while collecting less tax revenue.

Proposed “Transition Economy Acts” call for deficit spending and “inference compute taxes” to fund direct transfers. More radical “Shared AI Prosperity Acts” attempt to give citizens claim-rights on intelligent infrastructure returns, structured as dividends to households.

Opposition is fierce. “Occupy Silicon Valley” protesters blockade Anthropic and OpenAI’s San Francisco offices for three consecutive weeks.

The Speed Asymmetry

The core variable is speed. AI capability evolves by the quarter; institutional adaptation moves by legislative calendar.

The public needs confidence in the future. Policy often delivers division and hesitation.

What Citrini’s Scenario Gets Right

This thought exercise is valuable not because it predicts the future, but because it stress-tests an assumption that’s been dangerously underexamined:

When intelligence shifts from scarce to abundant, how do social and financial systems revalue human contribution, rebuild consumption and tax bases, and redirect output back into circulation?

The scenario captures several uncomfortable truths:

-

Individual optimization can be collectively catastrophic. Every company’s AI investment makes sense in isolation, even as systemic demand collapses.

-

Traditional recessions have natural brakes—this doesn’t. Falling demand usually reduces investment; here it accelerates it.

-

The speed asymmetry is real. Frontier AI capabilities compound quarterly. Policy debates stretch across election cycles.

-

Financial contagion paths are already built. The same securitization chains that transmitted subprime risk in 2008 now carry exposure to white-collar income assumptions baked into mortgages, private credit, and insurance reserves.

-

The “Ghost GDP” problem is genuine. As Citrini notes, a GPU cluster in North Dakota can replace 10,000 Manhattan white-collar workers’ output, but machines don’t buy cars, renovate homes, take vacations, or order drinks at restaurants. When monetary velocity stalls, consumption-driven economies wither.

-

The reflexive loop has no natural brake. Unlike past disruptions where falling demand curtailed investment, here reduced consumption incentivizes more AI adoption, accelerating the cycle.

Critical Counterpoints Worth Considering

That said, some countervailing forces deserve consideration:

-

AI might create new consumption categories we can’t yet imagine—much as smartphones created app economies and social platforms that employ millions

-

Policy response could be faster than modeled if crisis becomes acute enough to force action (though historical precedent suggests caution here)

-

International competitive dynamics may prevent full “race to zero” on employment if nations realize simultaneous domestic demand destruction creates mutual vulnerability

-

New forms of value capture may emerge—perhaps around curation, taste, trust, or human certification in an AI-abundant world

-

The transition timeline may be longer than this compressed scenario suggests, allowing more gradual adaptation and new equilibria to form

-

Historical disruptions created more jobs than they destroyed—though the lag time and skill mismatch caused severe transitional pain

The Canary in the Coal Mine

What makes Citrini’s scenario truly unsettling is that early-stage signals are already visible:

- Software companies are indeed cutting staff while reporting productivity gains

- Agent capabilities are advancing faster than most anticipated

- The “build vs. buy” conversation is entering enterprise procurement

- Private credit valuations are indeed lagging public market repricing

- Labor share of income has been declining for years

- Token consumption is exploding as AI becomes ambient

The full crisis may not unfold exactly as modeled. But the mechanism—reflexive feedback loops between capability, employment, consumption, and investment—is demonstrably real.

The Question We Must Answer

Citrini Research concludes their analysis with a reflection worth repeating in full:

“Looking back, the ‘Global Intelligence Crisis’ was more like a stress test of a long-ignored assumption: when intelligence shifts from scarce to abundant, how do society and financial systems revalue human worth, rebuild consumption and tax foundations, and return output to circulation? Repricing brings pain, but doesn’t necessarily mean collapse—new equilibria can still emerge. The difficulty lies in whether humanity can learn to negotiate and rewrite the rules faster when facing time.”

The question isn’t whether this scenario is correct.

The question is: if it’s even 30% correct, are we prepared?

Right now, the answer appears to be no.

The speed at which AI capabilities are advancing has outpaced our institutional capacity to adapt. Companies are optimizing at the firm level while destroying value at the system level. Financial structures built on decades of white-collar income stability are suddenly vulnerable. Policy frameworks designed for cyclical employment shocks face structural displacement.

As Citrini powerfully demonstrates, we may be racing toward an economic crisis not despite AI’s success, but because of it.

Full Source: Citrini Research & Alap Shah - “THE 2028 GLOBAL INTELLIGENCE CRISIS: A Thought Exercise in Financial History, from the Future”

This analysis serves as a critical examination of systemic economic risks identified by Citrini Research, not an independent forecast. The scenario presented functions as a stress test for assumptions embedded in current policy, financial underwriting, and corporate strategy. The timeline and magnitudes are speculative; the mechanisms warrant serious consideration.